Why PE-Backed Companies Need a Different Kind of Executive Search

Private equity does not give you time to figure leadership out. The moment a deal closes, the value creation plan is already running. Revenue targets, operating changes, and board expectations start immediately.

In that environment, a bad executive hire does more than slow things down. It delays execution, drains momentum, and puts direct pressure on the investment thesis.

The risk is larger than most companies plan for.

Research notes that 40 to 50% of new leaders fail within the first 18 months. In a PE-backed company, this kind of failure rarely stays contained to one function.

It erodes board confidence, disrupts teams, slows the value creation plan, and forces sponsors to spend precious time correcting a leadership decision that was supposed to accelerate performance.

That is why executive hiring in private equity works differently. Credentials matter less. What matters is whether someone can deliver inside the exact conditions your deal demands.

In this article we’ll cover:

Where traditional search falls short in PE

What a PE-ready leader actually looks like

How to align hiring with the investment thesis

Why specialized PE search firms perform better

How to assess candidates for real PE performance

What drives success after the hire

Still unsure if your next executive hire can actually deliver under PE pressure, or just look strong on paper? Alpha Apex Group helps you identify leaders who align with your deal thesis and execute from day one. Contact us to secure the right leadership for your portfolio.

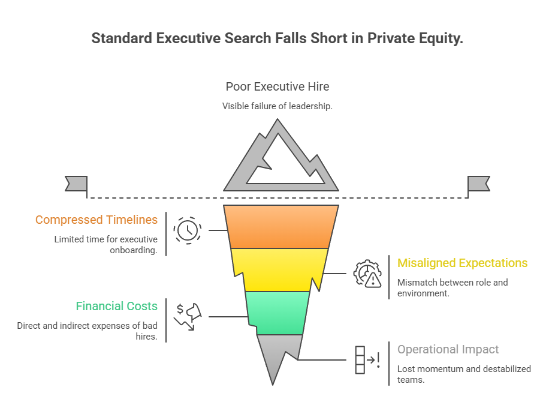

Why Standard Approaches Fail in Private Equity Executive Search Strategy

Standard executive search falls short in private equity because it was not built for the speed, pressure, or performance demands of a PE-backed company. Traditional search works reasonably well for large organizations with longer planning cycles, deeper infrastructure, and more tolerance for a slow ramp.

Portfolio companies operate differently. They need executives who can create impact quickly, work within a tightly defined investment thesis, and perform under close board scrutiny from day one.

When the search process is built for a different environment, the result is often a leadership match that looks right on paper but fails where it matters most.

Compressed Timelines Leave No Room for Slow or Wrong Hires

Here's what you're working with. The executive search process averages 4-6 months globally, and that's just to reach an offer. In a traditional enterprise with long planning horizons, that's uncomfortable but survivable.

In a PE-backed company, this timeline represents a significant chunk of the value creation runway consumed before the executive walks in the door.

And that's only if the hire works.

You need leadership teams that can execute from the first month, not the sixth. EBITDA growth targets, operational improvements, and go-to-market initiatives don't wait for an acclimation period. The investment thesis is already running.

During that delay, the business is still expected to move forward:

Revenue targets continue to build pressure

Operational gaps remain unresolved

Strategic initiatives stall without clear ownership

Board expectations do not slow down

A generalist executive search firm that runs the same process for a CRO at a portfolio company as it does for one at a Fortune 500 isn't calibrated to this reality. The role looks similar on paper. The performance environment is completely different.

A Wrong Executive Hire Drains Time, Money, and Momentum

Research shows the typical timeframe to identify, exit, and replace a poor executive hire runs 12 to 18 months. In a five-year hold period, that's potentially a third of the entire investment window consumed by a single personnel mistake.

The direct costs are real:

Severance packages

Recruiter fees

Compensation paid during underperformance.

But the indirect costs are much worse:

Lost momentum across the value creation plan

Declining board confidence

Teams losing direction and stability

Competitors gaining ground while you reset

For a sponsor working toward a defined return target, none of that time comes back.

This is why PE portfolio executive hiring can't be treated as a standard HR function. The stakes are higher, the timelines are tighter, and the consequences of getting it wrong compound quickly.

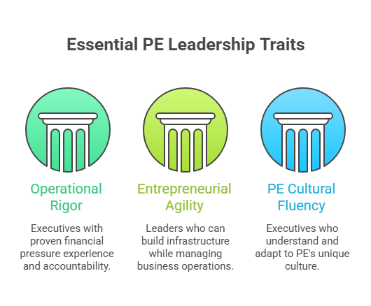

What the Right Leadership Profile Looks like in a PE-Backed Company

Before you build an executive search process that works in private equity, you need to be clear on what you're actually looking for. The mistake most sponsors make is starting with a job description that looks like every other C-suite brief.

From what we have seen, this is where most teams mess up. They define the role too broadly, then try to fix the mismatch later during interviews.

A strong PE leadership profile is specific. It comes down to three dimensions that need to be defined clearly before the search even begins..

1. Delivering Results Under Real EBITDA Pressure

The baseline requirement is an executive who has operated under genuine financial pressure.

In our experience, working with different portfolio companies, this is the first place where strong-looking candidates fall apart. They have managed budgets, but they have not owned outcomes under pressure.

What you are looking for is someone who has:

Owned a number or a margin target

Reported directly to a demanding board, and

Delivered results consistently.

According to Bain, deals that once needed only 5% annual EBITDA growth now require 10 to 12% to hit the same return. This shifts the operator profile required in a meaningful way.

Corporate executives who have spent careers in large enterprise environments have credentials that look right on paper. But large enterprises absorb underperformance in ways that portfolio companies cannot.

The executive you need has been accountable for operational results in real time. They have worked without the buffer of long planning cycles or the luxury of delayed execution.

2. Building Infrastructure While Running the Business

This is the differentiating trait that separates genuinely PE-ready executive talent from accomplished operators who will struggle in a portfolio environment.

According to Heidrick and Struggles, PE firms cite leadership as the number one value creation lever, 60% more often than efficiency or growth.

Most large-company executives have inherited infrastructure, teams, and systems. In a portfolio company, particularly one in a growth or turnaround phase, the executive is usually building the plane while flying it.

You are asking someone to build systems, hire teams, and drive execution at the same time.

Note: This requires a decision-making tolerance that cannot be assumed from a strong corporate track record. It has to be assessed directly.

3. Handling the Pressure of a PE Environment

This is where even genuinely talented operators get stuck.

According to Hogan Assessments, approximately 6 out of 10 CEO replacements in PE portfolio companies occur within the first year post-acquisition.

Most failures come down to lack of urgency, focus, or adaptability. This is a cultural alignment failure instead of a competence gap.

PE culture is accountability-heavy, data-driven, and board-facing in ways that catch experienced leaders off guard. Emotional intelligence matters here, specifically the ability to build relationships with sponsors quickly and communicate clearly under pressure.

Pro tip: The executives who succeed in portfolio companies usually understand these dynamics before they walk in the door. Cultural fit is a performance variable that needs to be assessed explicitly.

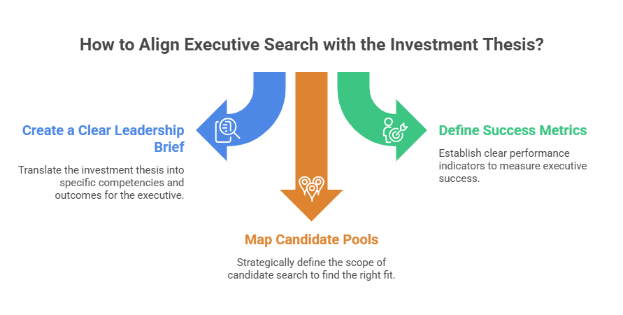

How to Align Private Equity Executive Search with the Investment Thesis

A search process without a strategy behind it is just a hiring exercise. In PE, where the investment thesis defines everything from operational priorities to the exit timeline, the executive search has to be built around that thesis from day one.

This means making three decisions before a single candidate is contacted.

1. Turn the Deal Thesis into a Clear Leadership Brief

The leadership brief coming from a standard HR process does not work in a PE context. It focuses on responsibilities instead of outcomes.

In our experience, the brief needs to translate the investment thesis directly into what the executive must deliver. That includes specific competencies, non-negotiables, and the true scope of the role.

The requirements change depending on the deal.

A growth thesis needs someone who can scale revenue quickly with limited resources

A roll-up strategy requires integration experience across multiple acquisitions

A turnaround needs a leader who can cut, restructure, and rebuild at the same time

The brief has to reflect that with precision.

According to Bain, 71% of PE investments fall short of projected margins due to siloed due diligence, missing deal-model EBITDA forecasts by an average of 330 basis points.

We have observed the same issue in hiring. When the leadership brief is not anchored to the deal thesis, teams end up searching for a generic executive instead of the operator the investment actually needs.

2. Define Success Metrics Before the Search Begins

Most organizations agree that leadership matters. However, very few act on that belief in any formal way before a hire is made.

According to McKinsey, 94% of GPs believe portfolio company leadership contributes an average of 53% toward investment returns, yet only 8% commit capital to optimize it through formalized processes.

We have observed that this gap creates problems after the hire, not during the search.

You need to define what strong performance looks like early:

What the executive should achieve by month 6

What progress should look like by month 12

What outcomes are expected by month 24

This alignment between sponsors, the board, and the operating partner removes one of the biggest sources of friction. Everyone works from the same definition of success.

It also strengthens the hiring process. Candidates can be evaluated against clear outcomes, which makes the assessment more objective and grounded in real expectations.

3. Map Where the Right Candidates Actually Sit

Once the brief is built and success metrics are agreed upon, the next decision is how broadly or narrowly to define the candidate pools. This is a strategic scope decision instead of a sourcing one. It covers three things:

Which adjacent industries and functional backgrounds translate well into a portfolio environment

What company-stage experience is genuinely relevant to the specific growth thesis

How far outside the obvious talent pool to look without compromising on non-negotiables

According to research, approximately 40% of mid- to large-cap PE funds lack dedicated talent management teams entirely.

This means the market intelligence and market research required to map candidate universes accurately often isn't sitting inside the firm. It has to come from search partners with real-time visibility into executive movement across sectors.

Why Specialized PE Search Firms Outperform Generalists in Portfolio Hiring

Specialized PE search firms outperform generalists because they are better at judging who can succeed in a PE-backed company.

They understand the pace, pressure, and performance demands of the role and are more likely to deliver a shortlist built for that environment instead of just a list of executives with strong resumes.

Access to Passive PE-Network Talent

Most generalist search processes rely on candidates who are already in the market. This is the limitation.

Job postings and broad outreach tend to reach executives who are actively looking. This is only a small and often unrepresentative portion of the available talent pool.

According to Hunt Scanlon Media, 85% of qualified executive candidates are not actively seeking new opportunities, and retained searches achieve a 71% placement rate.

This is where specialized PE search firms create an advantage. They have built long-term relationships with operators who have already worked inside portfolio companies and understand what the role demands.

Instead of running database searches, they reach out to candidates they already know. In many cases, these are executives they have placed in previous deals or followed over time.

This kind of access cannot be built quickly. It comes from years of working inside the PE ecosystem.

There is another layer to this.

Senior executives considering a move into a portfolio company need to trust the person presenting the opportunity. This trust depends on the search partner’s credibility and their understanding of how the business actually operates.

People Analytics and AI-driven Discovery Layered on Network Depth

Relationship-based sourcing remains the foundation of effective PE executive search. But leading firms now layer predictive analytics and technology on top of that foundation to sharpen time-to-shortlist without sacrificing candidate quality.

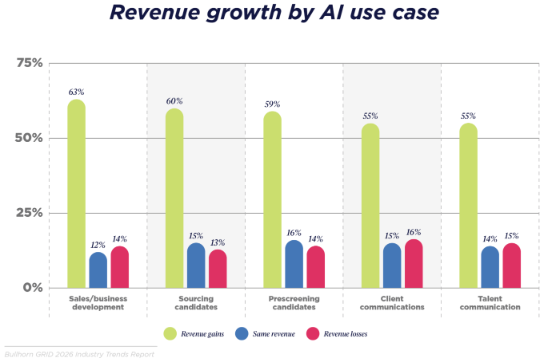

According to Bullhorn’s 2026 Recruitment Industry Trends Report, firms using AI at any stage of the recruitment process were 3.5 to 4.5 times more likely to have grown revenue, while 55% reported KPI improvements of more than 25% from AI screening alone.

And here are some other notable stats from the same report:

In a PE context, data helps narrow the field faster. It can surface executives who align with a specific growth thesis, even if they are not actively considering a move.

However, data alone does not close the gap.

In our experience, the real value comes from how that insight is used. The data highlights the right profiles, but relationships are what bring those candidates into a serious conversation.

Generalist firms usually lean on one side of this. Strong PE-focused search firms combine both, which is why their shortlists tend to be more relevant and more actionable.

How to Assess Candidates for Real PE Performance

The brief is written, the candidate universe is mapped, and the search firm is engaged.

Now comes the part that most processes get wrong. Assessment in a PE context has to be built for PE-specific outcomes, not adapted from a corporate hiring template.

Remember: the evaluation approach matters as much as the sourcing.

Use Real Scenarios to Test How Candidates Perform

Generic behavioral interviews don't surface what you actually need to know about a candidate in a PE context.

When you ask someone to describe a time they led a team through change; it tells you very little about how they'll perform when a board is demanding answers on a missed EBITDA target at month seven.

The interview process has to be structured around situations that actually predict PE performance. This means scenarios built around:

Rapid headcount decisions

Communicating bad news to a board under pressure

Executing a strategic pivot with limited resources and no time to build consensus

According to SIOP research, structured interviews carry a mean validity of .42 for predicting job performance, outperforming both cognitive ability tests and unstructured conversations.

Insider tip: The scenarios also have to be calibrated to the specific deal type. A competency framework built for a growth equity search looks different from one designed to assess a turnaround operator.

The questions, the scoring criteria, and the red flags you're watching for all differ. Using a one-size-fits-all assessment template across deal types is one of the most common failures in PE executive hiring, and one of the easiest to fix with the right search partner.

You can find more details about structured interviews in the video below:

Add Behavioral Data to Catch Risk Early

In our daily practice, we have noticed that structured interviewing alone isn't enough for the highest-stakes placements.

You need to integrate behavioral assessments directly into the process, and in some cases starting that work before a deal closes.

This shift toward pre-deal leadership due diligence reflects a broader understanding that leadership risk is deal risk.

According to Hogan Assessments, leaders who scored highly on Hogan assessment profiles were f5 times more likely to be rated as high performers and 8.4 times less likely to exhibit counterproductive behaviors after promotion.

For sponsors protecting enterprise value, this kind of predictive analytics insight changes how much capital should go into pre-hire evaluation.

The most effective assessment stacks typically combine:

Personality and risk profiling through tools like Hogan or the Predictive Index.

Competency-based scoring tied directly to the PE-specific scenarios from the interview process.

Structured reference checks that go beyond confirmation and probe for performance under pressure.

This combination gives a clearer view of how a candidate will perform. It helps you move beyond interviews and make more confident decisions.

How to Manage Private Equity Executive Onboarding, Retention, and Exit Planning

Hiring the right executive is only the starting point. What happens next determines whether that decision delivers.

In our experience, this is where many teams lose momentum. Onboarding, retention, and succession are often treated as secondary. In PE, they directly affect value creation.

| Stage | Focus | What Needs to Happen |

|---|---|---|

| First 100 days | Execution ramp | Align stakeholders, define early wins, reinforce success metrics |

| During hold period | Retention and alignment | Tie incentives to outcomes, maintain board alignment, track performance |

| Pre-exit | Readiness and depth | Fill leadership gaps, build succession, align team with exit strategy |

1. Set Up the First 100 Days for PE Environments

The first 100 days framing is a useful concept but a misleading benchmark.

According to McKinsey, 92% of externally hired leaders take significantly longer than 90 days to reach full productivity. In a PE environment where every month of ramp-up delays the value creation plan, that gap is expensive.

PE onboarding has to be more intentional and faster than what most corporate environments provide. And a structured executive integration significantly accelerates the path to full contribution.

A well-structured plan covers several priorities from day one.

Early win identification directly tied to the value creation plan already in motion

Stakeholder mapping across the sponsor, board, and operating partner before month one ends

Board relationship development treated as a structured activity, not an organic process

Clear reinforcement of the success metrics the executive agreed to pre-hire

Skipping or shortcutting any of these steps doesn't save time in the long run.

2. Keep Leaders Aligned Through the Hold Period

Hiring top executive talent is only the first problem. Keeping them aligned through the full hold period is the second.

According to AlixPartners, 86% of CEO turnover in PE portfolio companies is driven by the PE firm rather than the executive. Involuntary departures dominate, which means proactive retention planning matters far more than most sponsors acknowledge until it's too late.

Strong retention comes from clear incentives:

Meaningful equity tied to outcomes

Milestone-based rewards linked to the investment thesis

When an executive's upside is aligned to the same outcomes the board is targeting, engagement holds through difficult periods.

Retaining the wrong leader with golden handcuffs is just as costly as losing the right one early. The structure has to be designed with that reality in mind from day one.

3. Plan for Exit from Day One

Every leadership decision gets evaluated at exit.

From what we have seen, teams that delay succession planning pay for it later. Gaps in leadership reduce confidence and can affect valuation.

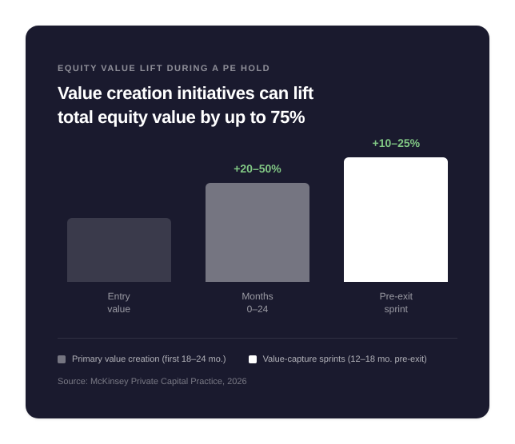

According to McKinsey, value creation initiatives in the first 18 to 24 months of a hold can lift equity value by 20 to 50%. This makes early leadership decisions the ones that carry the most weight.

Strong sponsors plan early:

Build leadership depth during the hold period

Align roles with the expected exit path

Ensure the team is complete before diligence begins

Early decisions carry the most weight. That is where value is either protected or lost.

Secure PE-Ready Leadership with Alpha Apex Group

Executive hiring in private equity directly affects how quickly a portfolio company can execute and deliver on its investment thesis.

The difference comes down to selecting leaders who can perform under pressure, not just those with strong credentials. This is why the search process needs to stay tightly aligned with the deal, the operating context, and the outcomes expected.

For firms facing this challenge, Alpha Apex Group offers a private equity-focused approach to executive search built around speed, fit, and long-term value creation.

If you need help identifying and securing the right leadership talent for a PE-backed business, we are equipped to support that work with the depth and rigor the process demands.

Reach out to us today to get started.

Frequently Asked Questions

Which executive roles do PE firms prioritize hiring first after an acquisition?

CEO and CFO are usually addressed first because they shape execution and board alignment. After that, hiring follows the deal thesis, such as CRO for revenue growth or COO for operational improvement.

How do management incentive plans work in PE-backed companies?

MIPs give executives equity tied directly to exit outcomes, along with milestone-based incentives. This structure aligns leadership with investor returns and can deliver higher upside than standard corporate compensation when the deal performs.

How do you attract senior executives to a PE-backed company?

Equity upside is a major driver, with the potential for meaningful long-term returns. Many executives also value faster decision-making, greater ownership, and a more direct link between performance and outcomes.

What happens to the executive team at exit?

Leadership is closely reviewed during diligence, and strong performers are often retained. Any gaps or misalignment within the team can reduce buyer confidence and impact valuation.

Research Appendix

- McKinsey & Company — It Really Isn't About 100 Days

- Altios — Executive Search Process Timeline: The 6-Month Reality No One Wants to Hear

- Pinnacle Search — The Hidden Cost of a Bad Executive

- Bain & Company — Welcome to a New Era: Global Private Equity Report 2026

- Heidrick & Struggles — Closing the Leadership Gap in Private Equity

- Hogan Assessments — How to Identify Leadership Potential in Private Equity Acquisitions

- Bain & Company — Integrating Due Diligence to Build Lasting Value

- McKinsey & Company — CEO Alpha: A New Approach to Generating Private Equity Outperformance

- Russell Reynolds Associates — Increased Focus on Strategic Talent Management for Value Creation

- Hunt Scanlon Media — Why Executive Search Firms Remain Essential for High-Stakes Leadership Hires

- Bullhorn GRID — 2026 Staffing & Recruiting Industry Trends Report

- SIOP — Is Cognitive Ability the Best Predictor of Job Performance? New Research Says It's Time to Think Again

- Hogan Assessments — Private Equity Spotlight

- AlixPartners — 10th Annual PE Leadership Survey

- McKinsey & Company — Beating the Odds: How Private Equity Firms Can Improve Exit Prospects